Last updated on April 12, 2026

Understanding personal income tax in Thailand is essential for every expatriate living in the Kingdom. Whether teaching English in Bangkok, running a business in Phuket, or retiring with a Thai spouse in Isaan you need to know. The Thai tax system directly affects financial planning and legal compliance. This comprehensive guide covers everything from tax residency rules to the 2024 foreign income remittance changes, deductions, filing procedures, and tax-saving strategies.

Table of Contents

What Is Tax Residency in Thailand?

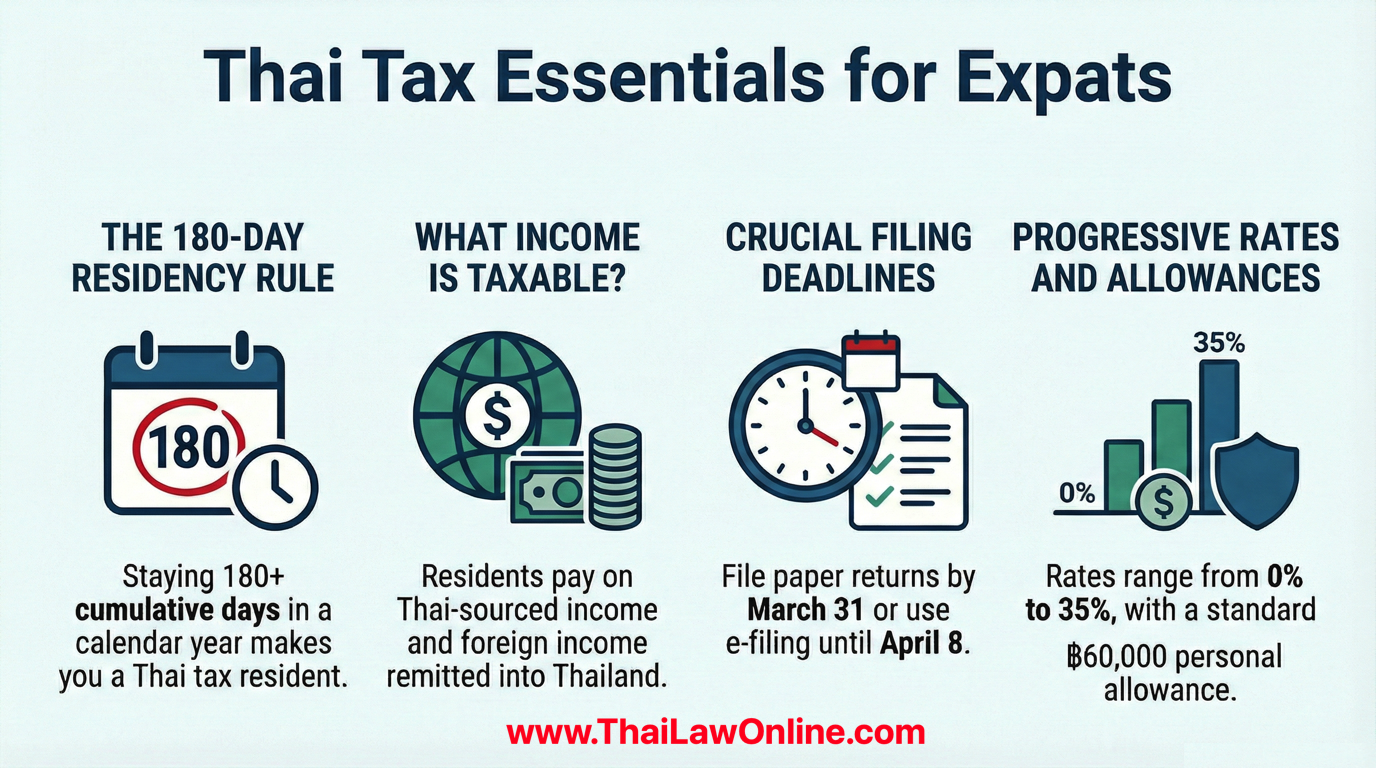

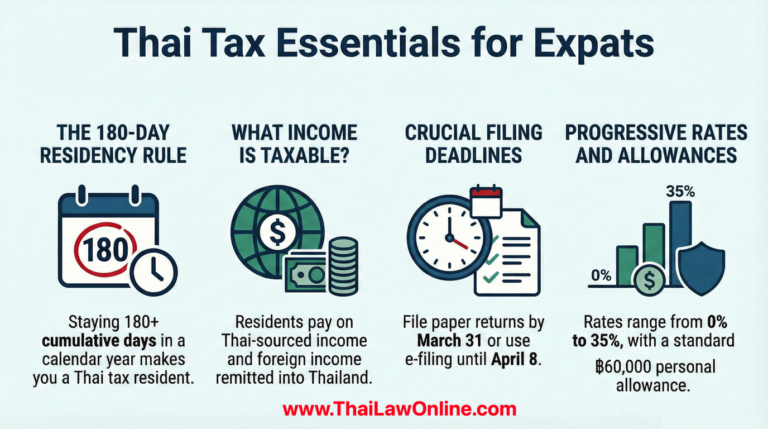

Tax residency in Thailand is determined solely by physical presence, not by visa type, nationality, or immigration status. Under Section 41 of the Thai Revenue Code, any individual who resides in Thailand for 180 days or more during a calendar year (January 1 to December 31) qualifies as a Thai tax resident.

This classification has major implications:

- Tax residents are liable for personal income tax on all Thai-sourced income and on foreign-sourced income remitted into Thailand.

- Non-residents are taxed only on income sourced within Thailand, such as salaries from Thai employers or rental income from Thai property.

The 180-day count does not need to be consecutive. Every day spent inside Thailand counts toward the threshold, regardless of the visa held. Teachers, retirees, business owners, and digital nomads who exceed 180 days are all subject to the same residency rules.

Important

The Thailand Privilege (Elite) visa does not provide any tax exemption. It is essentially a tourist visa with VIP benefits. Holders who stay 180+ days remain full tax residents under standard rules.

The 2024 Foreign Income Remittance Rule (Por.161/2566)

What Changed on January 1, 2024

On September 15, 2023, the Thai Revenue Department issued Departmental Instruction No. Por.161/2566, fundamentally changing how foreign-sourced income is taxed in Thailand. The new rules took effect on January 1, 2024, and represent the most significant tax change for expatriates in decades.

Before 2024: Thailand only taxed foreign-sourced income if it was remitted to Thailand in the same calendar year it was earned. This created a simple tax planning strategy — earn abroad, wait until the following year to transfer money, and it arrived tax-free.

From January 1, 2024: All foreign-sourced income remitted to Thailand by a tax resident is now taxable, regardless of when it was earned. The year the money enters Thailand triggers the tax, not the year it was earned abroad.

Pre-2024 Income Protection (Por.162/2566)

On November 20, 2023, the Revenue Department issued Departmental Instruction No. Por.162/2566, providing critical grandfathering protection. Any foreign income earned before January 1, 2024 remains entirely exempt from Thai tax, even if remitted after that date.

To claim this protection, expats should:

- Maintain separate bank accounts for pre-2024 and post-2024 funds.

- Preserve bank statements from December 2023 showing account balances as proof.

- Keep records of when income was earned (pay stubs, invoices, pension statements).

- Understand that the Revenue Department applies a FIFO (First-In, First-Out) method — older funds are assumed spent first.

What Counts as a “Remittance”

The definition of remittance is broader than many expats realize. The following methods all trigger a taxable remittance:

| Remittance Method | Example | Taxable? |

|---|---|---|

| Bank wire transfers | Sending money from a US/UK bank to a Thai bank account | Yes |

| ATM withdrawals | Using a foreign debit card at a Thai ATM | Yes |

| Credit/debit card payments | Paying for goods in Thailand with a foreign card | Yes |

| Physical cash | Carrying foreign currency across the border | Yes |

| Cryptocurrency conversion | Moving crypto to a Thai exchange and converting to THB | Yes |

| Online payment platforms | PayPal or Wise transfers to a Thai bank account | Yes |

What does NOT count as remittance:

- Foreign income kept entirely offshore (never brought into Thailand).

- Income earned before January 1, 2024, with proper documentation.

- Remittances made during years when the individual is not a Thai tax resident.

Proposed Two-Year Remittance Tax Exemption (Pending)

In June 2025, Deputy Director-General Panuwat Luengwilai announced that the Revenue Department was drafting legislation to ease the foreign income tax burden. Under the proposal, foreign-sourced income earned from 2024 onward would be exempt from tax if remitted within two calendar years — meaning in the year earned or the following year.

The two-year window (remit in earned year or next without tax) is still pending approval and could apply retroactively if passed. As of March 2026 when this article was written, this is under legislative review post-election.

Current Status: NOT Enacted

As of March 2026, this proposal has not been enacted into law. Following the dissolution of the House of Representatives, all pending legislative matters — including this exemption — are effectively paused. General elections were set for February 8, 2026, and no further updates are expected until a new government is formed.

Warning

Tax residents should not rely on this proposal for their 2025 tax filings. Plan and file based on the current rules until the exemption is officially published in the Royal Gazette.

Eight Categories of Assessable Income in Thailand

The Thai Revenue Code (Section 40) divides assessable income into eight categories. Correctly classifying income is important because different categories allow different standard deduction percentages. Here are the categories for personal income tax in Thailand

Personal Income Tax in Thailand – The Rates (2026)

Thailand applies a progressive tax system, meaning each portion of income is taxed at the rate for its respective bracket — not the entire income at a single rate. Both Thai nationals and foreign tax residents are subject to the same rate schedule.

How Progressive Taxation Works: A Practical Example for Personal Income Tax in Thailand

An expat earning a net taxable income of 500,000 THB does not pay 10% on the full amount. Instead:

- First 150,000 THB → Exempt = 0 THB. Filing is not mandatory below this if no tax due, though advisable for records.

- Next 150,000 THB (150,001–300,000) → 5% = 7,500 THB

- Next 200,000 THB (300,001–500,000) → 10% = 20,000 THB

- Total tax: 27,500 THB (effective rate of 5.5%)

Tax Deductions and Allowances

Maximizing legal deductions is the most effective way to reduce personal income tax in Thailand. The Revenue Code offers a wide range of personal allowances, insurance deductions, and investment incentives.

Personal and Family Allowances for Personal Income Tax in Thailand

Insurance and Retirement Deductions

Other Deductions for Personal Income Tax in Thailand

Other deductions include a domestic Tourism Deduction: A temporary 2025–2026 deduction (up to 20,000–30,000 THB for travel). Do note that you should really consult to know all of the deductions. Also, Thai ESG Fund deduction (up to 300,000 THB for investments through 2026, held 5+ years).

Double Taxation Agreements (DTAs)

Thailand has signed Double Taxation Agreements with 61 countries to prevent income from being taxed twice. These treaties have become more important than ever under the 2024 remittance rules.

How DTAs Protect Expats

DTAs work primarily through the foreign tax credit method: if tax has already been paid on income in the home country, that amount can be credited against the Thai tax liability on the same income. The credit is limited to the lesser of (a) the tax actually paid abroad, or (b) the Thai tax that would apply to that income.

On January 6, 2026, the Thai Revenue Department released an official Foreign Tax Credit Calculation Tool. This helps residents correctly compute their allowable credits when filing PND 90 or PND 91 returns.

Countries with a DTA with Thailand

Thailand’s 61 DTA partners include:

Asia-Pacific: Australia, Bangladesh, Cambodia, China, Hong Kong, India, Indonesia, Japan, Korea, Laos, Malaysia, Myanmar, Nepal, New Zealand, Pakistan, Philippines, Singapore, Sri Lanka, Taiwan, Vietnam

Europe: Armenia, Austria, Belarus, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Hungary, Ireland, Italy, Luxembourg, Netherlands, Norway, Poland, Romania, Russia, Seychelles, Slovenia, Spain, Sweden, Switzerland, Turkey, Ukraine, United Kingdom

Americas: Canada, Chile, United States

Middle East & Africa: Bahrain, Israel, Kuwait, Mauritius, Oman, South Africa, Tajikistan, United Arab Emirates, Uzbekistan

Special DTA Considerations for Common Expat Countries

- US Social Security: Generally taxable only in the US under the DTA, not in Thailand.

- Canadian state pensions (CPP/OAS): Typically taxable only in Canada.

- Australian government pensions: Generally taxable only in Australia.

- Private/employer pensions: Usually are taxable in Thailand if remitted, though credits for home-country tax may apply.

- US citizens: Due to a “Savings Clause” in the US-Thailand DTA, Americans should primarily use US mechanisms (Foreign Tax Credit or FEIE) to mitigate double taxation.

LTR Visa: Tax Exemption on Foreign Income

The Long-Term Resident (LTR) visa offers the most powerful tax benefit available to qualifying expatriates. Under Royal Decree No. 743, certain LTR categories receive a complete exemption from personal income tax on foreign-sourced income remitted into Thailand.

The exemption applies from the date the LTR visa is granted and remains valid while the visa is active. It does not apply retroactively to remittances made before visa approval.

Cryptocurrency and Digital Asset Taxation

Thailand has implemented a five-year personal income tax exemption on capital gains from cryptocurrency in Thailand and digital token disposals, effective from January 1, 2025, to December 31, 2029.

Key conditions for the exemption:

- Trades must be executed through SEC-licensed exchanges, brokers, or dealers in Thailand.

- The exemption applies to individuals only — companies remain subject to 20% corporate income tax.

- Capital losses can be deducted from capital gains when trading on licensed exchanges.

- OTC or unlicensed platform transactions remain taxable under standard progressive rates.

Proper documentation of all digital asset transactions during the exemption period is essential for future compliance when the tax holiday expires.

How to Get a Thai Tax Identification Number (TIN)

Every expat who needs to file taxes must first obtain a Tax Identification Number (TIN) from the Thai Revenue Department. Without a TIN, tax returns cannot be filed and certain banking or property transactions may be restricted.

Who Needs a TIN

- Employees with Thai employers (typically arranged by the company).

- Retirees, digital nomads, and freelancers who are tax residents and remit income.

- Foreigners selling property in Thailand.

- Business owners bringing foreign profits into Thailand.

How to Apply

- Prepare documents: Passport, visa or entry stamp, proof of address matching the TM30 registration.

- Complete Form L.P. 10.1 with personal details, nationality, passport number, and Thai address.

- Visit the district Revenue Office responsible for the residential address.

- Submit documents — officers will verify and, if everything matches, issue the TIN. Processing can be same-day in many offices.

Tip

The TIN application is free at any Revenue Office and typically takes 20–30 minutes. Bringing a Thai speaker is helpful as not all offices have English-speaking staff.

Filing Personal Income Tax in Thailand

Filing Deadlines

PND 90 vs. PND 91

- PND 91 is for taxpayers with employment income only (salary from a single employer).

- PND 90 is for taxpayers with multiple income sources. Examples, employment plus rental income, foreign remittances, investment income, freelancing, or business income.

Most expats with foreign income remittances will need to file PND 90.

How to File Online (E-Filing) for Personal Income Tax in Thailand

- Register at efiling.rd.go.th using the TIN and personal details.

- Log in and select the correct form (PND 90 or PND 91).

- Enter all income details for the tax year, including Thai-sourced and remitted foreign income.

- Input deductions: allowances, insurance premiums, donations, and retirement contributions.

- Review the tax calculation and submit.

- Pay any tax due via bank transfer, credit card, or QR code payment.

Penalties for Non-Compliance to Personal Income Tax in Thailand

Tax Planning Strategies for Expats in Thailand

1. Use Pre-2024 Funds First

Remit from accounts holding savings earned before January 1, 2024. Under FIFO rules, older funds are assumed to be spent first. Maintain clear documentation.

2. Manage Tax Residency Strategically

Staying under 180 days in Thailand during a calendar year means non-resident status and no tax obligation on foreign-sourced income. Monitor the day count carefully, especially when traveling in and out.

3. Maximize DTA Foreign Tax Credits

Claim credits for taxes paid in the home country using the Revenue Department’s new Foreign Tax Credit Calculator. Obtain a Certificate of Residence from the home country’s tax authority and include it with the Thai tax filing.

4. Maximize Thai Deductions

Take full advantage of the 60,000 THB personal allowance, spouse and child allowances, insurance premiums, and retirement fund contributions. These can significantly reduce the effective tax rate.

5. Consider the LTR Visa

For expats who meet the financial thresholds, the LTR visa provides a complete exemption from tax on foreign income. This can save hundreds of thousands of baht annually for high-income retirees and remote professionals.

6. Time Remittances for Lower Tax Brackets

In years with lower Thai-sourced income, larger remittances may fall into lower progressive tax brackets. Planning the timing of transfers can optimize the overall tax burden.

Common Mistakes Expats Make

- Mixing pre-2024 and post-2024 funds in a single account without documentation — the entire transfer may be treated as taxable.

- Overlooking ATM withdrawals and credit card payments as remittances — these transactions add up over the year and are taxable.

- Assuming proposed tax changes are law — the two-year grace period has not been enacted. File based on current rules.

- Not filing a return when income is below the taxable threshold — filing still creates a paper trail and avoids late filing penalties.

- Confusing Thailand Privilege (Elite) visa with LTR visa — only the LTR visa provides foreign income tax exemption.

- Ignoring Double Taxation Agreements — many expats overpay by not claiming foreign tax credits they are legally entitled to.

Frequently Asked Questions

Do I have to pay Thai tax on my foreign pension?

It depends on when the pension was earned and whether a DTA applies. Pension income earned from 2024 onward is taxable when remitted to Thailand. However, pre-2024 pension income is protected under Por.162/2566. Government pensions from countries like the US, Canada, and Australia are often exempt under their respective DTAs. Private pensions are generally taxable but may qualify for a foreign tax credit.

I use my foreign credit card for purchases in Thailand. Is that taxable?

Yes. Using a foreign credit or debit card for purchases inside Thailand is considered a remittance of foreign funds and is taxable under the 2024 rules. The same applies to ATM withdrawals using foreign bank cards. However, we have to be honest… tourists do it, lots of people do it. How will they apply this rule or be able to check people? It will be extremely difficult.

What is the difference between PND 90 and PND 91?

PND 91 is for individuals who only earn employment income (salary). PND 90 is for individuals with multiple income sources, including foreign remittances, rental income, investments, or business income. Most expats dealing with foreign income will file PND 90.

Can I file my taxes in English?

The Revenue Department’s e-filing system at efiling.rd.go.th has some English translation available, but the system can be challenging to navigate for complex situations. Engaging a Thai tax professional or filing service is advisable for expats with foreign income obligations.

Does the Thailand Elite visa give me any tax benefits?

No. The Thailand Privilege (formerly Elite) visa is a tourist visa with VIP services. It provides no tax exemptions whatsoever. If an Elite visa holder stays in Thailand for 180+ days, they are a full tax resident subject to standard rules. Only the LTR visa provides tax benefits on foreign income.

What happens if I earn crypto income in Thailand?

Capital gains from cryptocurrency and digital token sales are exempt from personal income tax from January 1, 2025, to December 31, 2029, under Ministerial Regulation No. 399. This exemption applies only to trades through SEC-licensed platforms and only to individuals. After 2029, crypto gains will revert to standard progressive tax rates unless the exemption is extended.

How do Double Taxation Agreements help me?

DTAs prevent the same income from being taxed in two countries. If an expat has already paid tax on income in the home country, a foreign tax credit can be claimed against the Thai tax liability. Thailand has DTAs with 61 countries. The Revenue Department released a Foreign Tax Credit Calculator in January 2026 to help taxpayers compute their credits.

What if I stay in Thailand less than 180 days?

Individuals who are physically present in Thailand for fewer than 180 days in a calendar year are not Thai tax residents. Non-residents are only taxed on income sourced within Thailand (e.g., a Thai employer salary). Foreign-sourced income, including remittances, is not taxed for non-residents.

When is the tax filing deadline for expats?

The annual personal income tax return must be filed by March 31 for paper submissions or April 8 for electronic filings through the Revenue Department’s e-filing portal. Late filing results in fines of up to 2,000 THB per month and a 1.5% monthly surcharge on any unpaid tax. Installment options for taxes are possible for over 3,000 THB (interest-free up to 3 months).

Is there a minimum income threshold for filing?

Tax residents whose net assessable income is 150,000 THB or less are exempt from paying personal income tax. However, filing a return is still recommended to maintain compliance records and avoid potential penalties.

Key Takeaways for Expatriates

Navigating personal income tax in Thailand requires awareness of the 2024 remittance rule changes, strategic use of deductions and DTAs, and timely filing. Expats should secure a TIN, understand which income categories apply, document pre-2024 funds carefully, and never assume that pending legislative proposals are already law. Professional tax advice tailored to individual circumstances remains the safest approach to compliance and tax optimization.

This guide is provided for informational purposes by ThaiLawOnline.com. Tax laws change frequently. Consult a qualified tax professional for advice specific to your situation.

Links about Personal Income Tax in Thailand: