Last updated on April 12, 2026

Value Added Tax (VAT) is Thailand’s main tax on things people buy. It applies to most goods and services sold in the country. Right now, the VAT is set at 7%. This rate was lowered from the standard 10% in 1997, impacting how businesses manage their output tax. VAT is an important part of Thailand’s tax system. It impacts both businesses and consumers. The rate of 7% is through 30 September 2026, following the Cabinet decision and Royal Decree now gazetted.

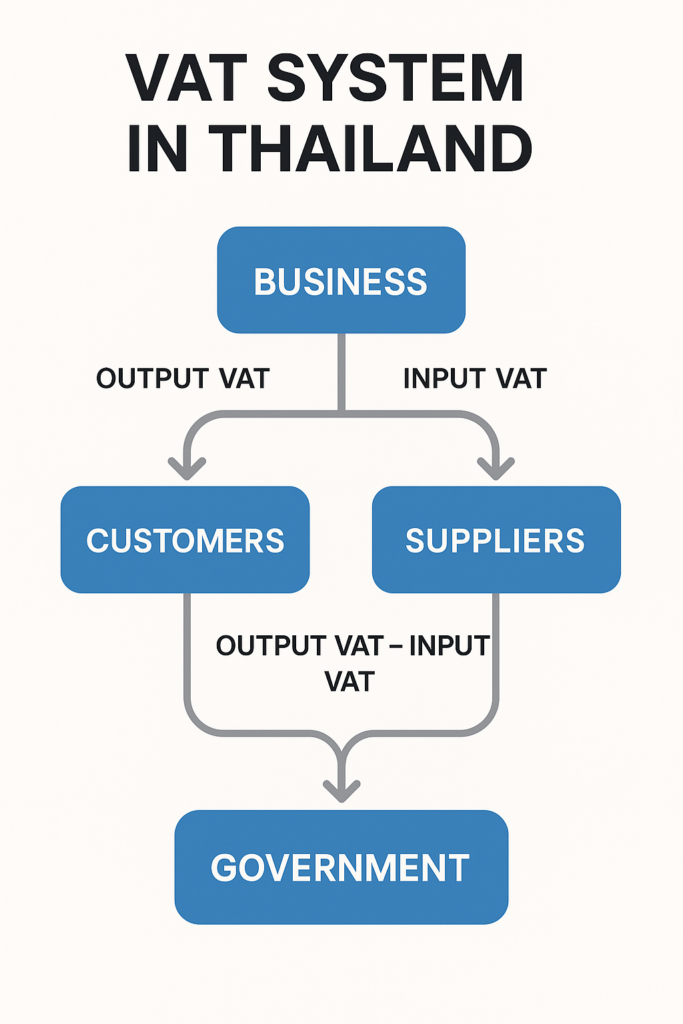

VAT Registration in Thailand works by allowing businesses to offset costs. They collect output VAT from customers when selling goods or services. They also pay input VAT on their business purchases. The difference between these amounts shows if a business owes VAT to the government or can get a refund.

Foreign businesses and expatriate entrepreneurs in Thailand need to understand VAT registration and compliance, especially regarding services rendered in Thailand. This knowledge is essential for staying legal and avoiding costly penalties. These penalties can greatly affect business profits.

Table of Contents

Mandatory VAT Registration in Thailand : Requirements

VAT Registration and Filing in Thailand – Quick Reference Table

| Requirement | Details |

|---|---|

| Standard VAT Rate | 7% (reduced from 10% since 1997) |

| Mandatory Registration Threshold | Annual revenue over 1.8 million THB |

| Foreign Businesses | Must register if providing services in Thailand or digital services to Thai consumers (no physical presence needed) |

| Import/Export Companies | Must register regardless of revenue |

| Voluntary Registration | Allowed below threshold, but deregistration requires 1 year minimum and Revenue Department approval |

| Required Form | VAT Registration: PP.01 (or PP.01.1 for voluntary); Monthly Filing: PP.30 |

| Filing Deadlines | Paper filing: 15th of following month; E-filing: 23rd of following month |

| Penalties | If you do not file on time, you may face a fine. This fine can be up to twice the VAT you owe. You will also have to pay a 1.5% monthly fee on any unpaid VAT. |

| Exemptions | Agriculture, education, healthcare, domestic transport, property rentals, charitable and religious services |

| Zero-Rated Transactions | Exports, international transport (air/sea), free trade zones, services to international carriers |

Annual Revenue Threshold

Any person or business doing taxable activities in Thailand must register for VAT. This is required when their yearly income is over 1.8 million baht. This threshold applies to both Thai and foreign businesses operating within the Kingdom. You must complete registration within 30 days of reaching this threshold. This applies no matter when it happens during the tax year.

Foreign Business Requirements

Non-resident businesses face different registration requirements depending on their activities in Thailand. Foreign companies that offer digital services to Thai consumers must register for VAT. Threshold is 1.8 million baht per calendar year or accounting period. Filing and payment are due by the 23rd of the following month under the TRD’s e-services system. It does not matter if they are physically in the country. They still need to register for VAT if they provide services in Thailand.

Companies that bring goods into Thailand must register for VAT. This includes companies that set up or assemble imported products. It also applies to those that export goods. There is no minimum threshold for this requirement. This rule makes sure that foreign businesses in Thailand pay VAT. This way, they can compete fairly with local companies.

Work Permit Dependencies

A key requirement for foreign investors is often overlooked. Companies that want to hire foreign workers must “normally” maintain their VAT registration. This rule applies to businesses with revenue below the registration limit. Most foreign-owned businesses in Thailand must register for VAT. They must follow VAT rules. It is not strict and can vary from a province to another.

Voluntary Registration Benefits

Businesses operating below the mandatory threshold may choose voluntary VAT registration to claim input VAT credits on business expenses. This option proves particularly advantageous for companies with significant startup costs, imported equipment, or substantial business-to-business transactions with VAT-registered suppliers.

However, voluntary registration requires careful consideration as deregistration proves difficult once established. Businesses must maintain registration for at least one year and demonstrate compelling reasons for cancellation to revenue authorities.

VAT Registration in Thailand : Process and Documentation

Required Documentation

The VAT registration process requires comprehensive documentation to establish business legitimacy and operational capacity. Essential documents include the completed VAT Registration Application Form (PP.01 or PP.01.1 for voluntary registration) in triplicate, signed by authorized company representatives.

Proof of business location is very important. You need lease agreements with the right stamp duty or letters from the owner for business use. House registration documents for the business premises, along with property ownership documentation from lessors, must accompany location proof.

You also need to provide detailed maps that show the exact location of your business. Include photographs of your business premises that show the company signage and the interior office space. Lastly, submit copies of your incorporation certificates along with your complete business objectives.

For foreign-owned companies, directors must provide passport copies, visa documentation, and work permit details with authorized signatures. Power of attorney documentation with stamp duty becomes necessary when representatives handle registration procedures.

Registration Procedures

Businesses in Bangkok must submit applications to the Area Revenue Branch Offices. Companies in other provinces apply through their local Area Revenue Branch Offices. The Revenue Department has streamlined this process by allowing simultaneous VAT registration with company incorporation through the Department of Business Development since April 2020.

Online registration has become increasingly available, though many businesses prefer working with qualified Thai accounting firms to ensure proper completion and submission. The usual registration process takes 4 to 6 days to prepare and file documents. VAT certificates (PP.20) are issued within 45 working days.

Upon approval, businesses must display their VAT registration certificates prominently at registered business locations alongside company registration documentation. Failure to display required certificates can result in compliance penalties during revenue inspections.

Monthly Filing Requirements

PP.30 Return Form

All businesses that are registered for VAT must file monthly VAT returns. They should use Form PP.30, even if they did not make any money that month. This requirement applies universally – even businesses with zero sales must submit blank returns to maintain compliance.

The PP.30 form needs a clear report of output VAT collected from customers. It also requires input VAT paid on business purchases. Finally, it calculates the net VAT liability or refund amount. Businesses must maintain supporting documentation including original purchase invoices and copies of sales tax invoices for revenue department verification.

Monthly reporting periods follow calendar months, with returns due by the 15th of the following month (paper). It is the 23rd of the following month” for e-filing. The 8-day extension is now in effect until January 31, 2027. For example, report January VAT activity by February 15th. This deadline stays the same, even on weekends or holidays. Submissions due on non-working days can be accepted the next business day.

Electronic Filing Systems

Thailand has modernized VAT compliance through electronic filing systems that offer extended submission deadlines and improved convenience. Businesses that file electronically using the Revenue Department’s e-filing portal have a deadline. They must complete their returns by the 23rd of the following month.

The e-filing system supports document uploads, automatic calculations, and digital record-keeping that simplifies compliance management. Companies that handle many transactions can set up host-to-host connections for direct data transfer. This is especially helpful for businesses supervised by the Large Business Tax Administration Division.

Recent changes include required e-filing for some business types. There is also a new e-tax invoice system that works with VAT reporting rules. These digital systems enhance accuracy while reducing administrative burdens for compliant businesses. The government has a digital tax ecosystem goal by 2028. Approved e-tax invoices are using digital certificates and XML and that data is submitted monthly.

Supporting Documentation Requirements

Proper tax invoices remain fundamental to VAT compliance and must include specific information elements. Valid tax invoices must show full company names and addresses for both parties. They should include VAT identification numbers, clear transaction descriptions, and stated VAT amounts.

Input tax invoices maintain six-month validity for offsetting sales VAT, requiring businesses to manage their documentation timing strategically. Companies must retain all VAT-related records for five years to satisfy audit requirements and support refund claims.

Revenue authorities may request supporting documentation during filing or subsequent audits, making accurate record-keeping essential for sustainable operations. Digital record management systems increasingly support compliance while reducing physical storage requirements.

Penalties and Compliance Consequences

Late Filing Penalties

Thailand’s VAT penalty structure involves multiple penalty types that can accumulate rapidly for non-compliant businesses. Failing to file on time exposes the filer to a fine up to twice the VAT due and a 1.5% monthly surcharge on unpaid VAT.

More significant penalties apply to businesses with VAT liabilities. Late submission penalties can be as high as 200% of the VAT amount owed. There are also monthly fees of 1.5% on unpaid VAT. These fees apply from the due date until the payment is made. These penalties compound monthly, creating substantial financial burdens for delayed compliance.

Businesses submitting incorrect or incomplete returns face additional penalties equivalent to 100% of unpaid tax amounts. Repeated violations or intentional fraud can result in criminal charges with potential imprisonment and heavier court-imposed fines.

Administrative Consequences

Beyond financial penalties, VAT non-compliance creates operational challenges that can severely impact business activities. Companies that do not file PP.30 forms for six months will lose their VAT registration. They will need to re-register to continue operations and follow VAT rules in Thailand.

Immigration and work permit authorities scrutinize VAT compliance records when reviewing visa extensions and work permit renewals. Poor VAT compliance history can result in application rejections or increased scrutiny that delays essential business processes.

Revenue authorities have the right to do compliance audits. These audits can disrupt business operations and take a lot of management time and resources. Maintaining current VAT compliance significantly reduces audit risk and associated operational disruptions.

VAT Exemptions and Zero-Rated Transactions

Exempt Transactions

Certain business activities remain completely exempt from VAT requirements, regardless of transaction values. Agricultural products sales, including unprocessed agricultural goods, animals, fertilizers, and animal feed, maintain VAT exemptions that support Thailand’s agricultural sector.

Educational services from government schools and approved private schools are exempt from VAT. This shows the unique nature of services in Thailand. Healthcare services from government hospitals and licensed clinics also qualify. Professional services like medical care, auditing, and legal services could be also exempt.

Transportation services, particularly domestic land transportation and international transportation by land, remain exempt along with immovable property rentals, religious services, and charitable activities. These exemptions recognize essential services that benefit Thai society broadly.

Zero-Rated Transactions

Zero-rated VAT applies to specific international transactions that support Thailand’s export economy. Goods and services sold outside Thailand can get zero-rated treatment. This lets exporters claim input VAT refunds. It helps them stay competitive in international markets.

International transportation services by air and sea receive zero-rated status, as do services provided to international carriers operating in Thailand. Free trade zone activities intended for export manufacturing also qualify for zero-rated treatment under specific documentation requirements.

To claim zero-rated status, businesses must keep detailed records. These records should show foreign sales or exports. They must include proof of payment from foreign sources, shipping documents, and customs clearance records. Revenue authorities closely check documents for zero-rated claims. This is especially true when a VAT registrant does not provide enough proof.

Input VAT Credits and Refunds

Credit Mechanism

Thailand’s VAT system allows businesses to offset input VAT paid on business purchases against output VAT collected from sales. This credit mechanism prevents double taxation and ensures VAT applies only to value-added at each business level.

Eligible input VAT includes buying raw materials, business equipment, professional services, and other goods used for business. However, certain expenses like entertainment costs remain excluded from input VAT credit eligibility.

Input VAT credits maintain six-month validity from the invoice date, requiring businesses to claim credits within this timeframe. Unused credits can be used in later months during the validity period. This gives businesses with uneven cash flows more flexibility.

Refund Procedures

When input VAT exceeds output VAT, businesses become entitled to VAT refunds that can significantly improve cash flow. Exporters and zero-rated suppliers have guaranteed rights to refunds. Their sales create little output VAT but keep a lot of input VAT from business purchases.

Refunds are usually processed in three ways. For smaller amounts, you can get cash at revenue offices. For larger refunds, bank transfers are used. You can also receive tax credits for future VAT payments. Electronic filing systems have streamlined refund processing and reduced processing times.

Businesses must maintain comprehensive documentation supporting refund claims, including original tax invoices, export documentation, and evidence of business use for input VAT items. Revenue authorities may audit refund claims, making accurate documentation essential for successful refund processing, especially when input tax exceeds expectations.

Recent Developments and Digital Transformation

E-Tax Invoice Systems

Thailand’s Revenue Department has introduced voluntary e-tax invoice systems that streamline VAT compliance while enhancing government oversight capabilities. Two systems meet different business needs. The E-Tax Invoice & e-Receipt system is for larger operations. The E-Tax Invoice by Email system is for smaller businesses.

These systems require electronic certificates, digital signatures, and XML format submissions that integrate with monthly VAT reporting requirements. Implementation timelines suggest broader mandatory adoption by 2028, making early adoption strategically advantageous for competitive businesses.

Benefits include reduced document storage costs, faster processing times, and integration with accounting systems that improve accuracy and efficiency. However, implementation requires technical capabilities and certified service provider relationships that may challenge smaller operations.

Regulatory Updates

Recent regulatory changes reflect Thailand’s commitment to modernizing tax administration and closing compliance gaps. Foreign digital service providers now have stricter rules. They must submit and complete payments by the 23rd of each month.

The Revenue Department is still looking at ideas to lower the VAT registration limit below 1.8 million baht. This change could impact many small businesses that do not have to register right now. These changes would significantly expand the VAT-registered business base while increasing compliance burdens on micro-enterprises.

Digital transformation initiatives increasingly emphasize electronic filing and digital record-keeping that support efficient tax administration. Businesses investing in digital compliance capabilities position themselves advantageously for future regulatory requirements while improving operational efficiency in managing output tax.

Best Practices for VAT Compliance

Internal Systems

Successful VAT compliance requires robust internal systems that support accurate record-keeping, timely filing, and effective communication with revenue authorities. Businesses should implement accounting systems capable of tracking VAT transactions separately and generating required reports efficiently.

Monthly compliance calendars help meet deadlines. They also reduce last-minute filing pressure, which can cause errors and penalties. Regular internal reviews of VAT processes identify improvement opportunities and compliance gaps before they become significant problems, particularly for services rendered in Thailand.

Staff training on VAT requirements and documentation standards ensures consistent compliance across all business activities. This training should cover invoice requirements, record-keeping standards, and penalty awareness that motivates careful attention to compliance details.

Professional Support

Many businesses struggle with Thai VAT rules. These rules are complex, and there are strict penalties for not following them. This is especially true if a VAT registrant does not meet reporting requirements. Because of this, most businesses need help from qualified professionals. Thai accounting firms specializing in VAT compliance can provide registration assistance, monthly filing services, and advisory support that ensures ongoing compliance.

Professional support proves particularly valuable for foreign-owned businesses navigating language barriers and unfamiliar regulatory requirements. Qualified accountants can communicate effectively with revenue authorities and provide guidance during audits or compliance challenges.

The cost of professional support is usually a small part of possible penalties. It also offers peace of mind and helps businesses grow and make money.

Strategic Considerations

VAT registration and compliance should align with broader business strategies rather than representing mere regulatory obligations, especially for companies subject to VAT. Voluntary registration may support business expansion plans, supplier relationships, or competitive positioning in VAT-sensitive markets.

Cash flow management is very important for VAT-registered businesses. This is especially true for those who get regular refunds and those whose input tax is higher than their output tax. Strategic timing of major purchases and sales can optimize VAT positions and improve working capital management.

Long-term business planning should consider VAT implications of expansion activities, new product lines, or market entry strategies. Early consultation with qualified advisors ensures VAT considerations support rather than hinder business objectives.

FAQs about VAT Registration in Thailand

What is the current VAT rate in Thailand and who has to pay it?

Thailand’s Value Added Tax (VAT) is 7% (reduced from the standard 10% since 1997). It applies to most goods and services sold or used in Thailand, affecting both businesses and consumers. Businesses collect output VAT from sales. They can offset this with input VAT paid on purchases. The difference shows if VAT is payable or refundable.

When is VAT registration mandatory in Thailand (thresholds and timing)?

You must register if your taxable revenue is more than 1.8 million THB in a year or over. You must register within 30 days of reaching the threshold. Importers must register regardless of revenue. You can choose to register for voluntary VAT even if you are below the threshold. However, to deregister, you usually need to wait at least one year and get approval.

How do foreign companies and expat entrepreneurs handle VAT in Thailand?

Non-resident and foreign-owned businesses must register if they provide services in Thailand. They also need to register if they offer digital services to Thai consumers. This applies even if they do not have a physical presence. Registration is required once their Thai-sourced revenue exceeds the set threshold. Import or assembly activities also trigger registration with no minimum threshold. Maintaining VAT registration can be necessary for work permit and visa processes, so compliance directly supports immigration renewals.

What are the monthly VAT filing rules (PP.30), deadlines, and penalties?

All VAT registrants file Form PP.30 every month, even with no sales (file a nil return). Paper filing is due by the 15th of the following month; e-filing extends the deadline to the 23rd. Keep sales tax invoices, purchase invoices, and records for five years. Failing to file on time exposes the filer to a fine up to twice the VAT due and a 1.5% monthly surcharge on unpaid VAT.

What transactions are VAT-exempt or zero-rated, and how do refunds work?

Exempt: Agriculture, education, healthcare, domestic land transport, property rentals, and religious and charitable services do not have VAT. Input VAT cannot be credited.

Zero-rated (0%): This includes exports, international air and sea transport, free-trade zones, and services for international carriers. No VAT is charged, but input VAT can be credited or refunded. Input VAT credits generally have six-month validity from invoice date. If the input VAT is more than the output VAT, you can claim a refund using PP.30. Include supporting documents like tax invoices and shipping or customs proof. Refunds are given as cash for small amounts, bank transfer, or future tax credits.

VAT registration and monthly filing requirements represent fundamental obligations for most businesses operating in Thailand. These requirements are complex, but they help organize Thailand’s tax system. This system funds important government services and supports a competitive business environment. Success requires careful attention to registration requirements, accurate monthly filing, comprehensive record-keeping, and strategic professional support that ensures compliance while supporting business objectives.

Links:

Thai Law Updates, free by email

Plain-English updates on Thai law changes that affect foreigners: property, visas, marriage, business and wills. One short email a month from a firm practicing since 2006. No spam, unsubscribe anytime.