Last updated on April 12, 2026

Thailand’s beaches, affordable lifestyle, and welcoming culture attract thousands of foreigners every year looking to buy property in Thailand. But Thailand’s property laws are fundamentally different from what most Western buyers expect. Unlike Anglo-American common law systems that generally permit absolute fee simple ownership regardless of nationality, the Thai legal framework is built on a strict protectionist doctrine. And normally, foreigners cannot own land in Thailand. There are rare exceptions. Reality is personally doing that work since 2006, I never seen one foreigner owning land in Thailand as “owner” on a title deed. Never. Understanding the nuances of Buying Property in Thailand as a Foreigner is essential.

That doesn’t mean you can’t own property. It means you need to understand the legal structures available to you, and the very real risks of getting them wrong. Any circumvention of ownership restrictions, whether through unauthorized nominee structures, fraudulent financial declarations, or unapproved corporate holding mechanisms — carries severe civil and criminal penalties, including forced divestiture, substantial fines, and potential imprisonment.

This guide, based on over 30 years of practicing Thai property law for international clients, covers every legitimate pathway. For example, the outright freehold ownership of condominium units or sophisticated long-term leasehold structures can be done. Same as separating building ownership rights. Other specialized real rights such as usufructs and superficies are other ways to protect a real estate investment.

Table of Contents

For many, Buying Property in Thailand as a Foreigner opens up exciting opportunities, but being informed is key.

Understanding Buying Property in Thailand as a Foreigner

The Core Rule: Foreigners Cannot Own Land in Thailand

Two foundational statutes govern real property rights in Thailand: the Land Code Act B.E. 2497 (1954) and the Thai Civil and Commercial Code (CCC). Their interplay establishes the boundaries of what foreigners can and cannot do.

At the center of Thai property law is Section 86 of the Land Code Act. This statute explicitly dictates that aliens (foreigners) may only acquire land by virtue of a treaty granting the right to own immovable properties. As of 2026, there are no active treaties in effect that grant foreign nationals a general right to own land. The prohibition is functionally absolute, barring the narrow statutory exception of Section 96 bis (covered below). Violating Section 86 — either personally or through an agent — triggers penalties under Section 111 of the Land Code, including fines, imprisonment, and the mandatory forced sale of the land within a timeframe set by the Director-General of the Land Department.

Equally critical is CCC Section 1299, which governs the perfection of real rights. It states that no acquisition of immovable property, or any real right attached to it, is complete unless made in writing and formally registered by the competent official. This means private, unrecorded contracts about land, long-term leases, or usage rights are unenforceable against third parties. For foreign buyers, every legal instrument — whether a lease exceeding three years, a usufruct, or a superficies — must be registered at the Land Department and endorsed on the official title deed to guarantee legal protection. For a deeper analysis of foreign ownership restrictions in Thailand, see our dedicated article.

The “99-year lease” legislation widely discussed in 2025? Still not enacted. The proposed legislation to extend the maximum statutory lease term from 30 to 99 years was fast-tracked through parliamentary readings in late 2025, but until the bill receives final Royal Assent and publication in the Royal Gazette, legal practitioners advise relying exclusively on secure 30-year frameworks. The maximum registrable lease remains 30 years under CCC Section 1337. For a deeper analysis of long-term lease structures, see our article on the 90-year lease myth vs. reality.

What’s more, on March 18, 2025, the Thai Supreme Court issued a landmark ruling (Case No. 4655/2566) that permanently invalidated the common “30+30+30” lease renewal structure, ruling that pre-agreed renewal clauses for periods beyond the initial 30-year term are void and violate public policy. We covered this ruling in our analysis of Supreme Court decisions about leases in Thailand. If you signed a lease with this structure, you should seek legal advice immediately.

What Foreigners CAN Own: Your Legal Options

While foreigners cannot buy land in Thailand directly, several legal structures allow you to own or control property. Each has distinct advantages, limitations, and risk profiles.

1. Condominium Freehold — The Simplest and Safest Path

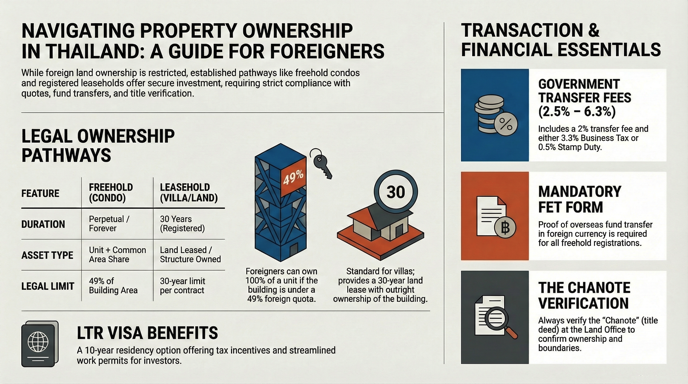

Under the Condominium Act B.E. 2522 (1979), foreigners can own a condominium unit in freehold — outright, permanent ownership with a title deed (Chanote) in their own name. This is the most popular and most secure option for foreigners buying a condominium in Thailand, provided:

- The building’s foreign ownership quota does not exceed 49% of the total unit floor area. This quota has not been raised to 75% despite government proposals — it remains at 49% as of March 2026. Before signing anything, your lawyer must verify the current ratio directly with both the building’s Juristic Person (management office) and the Land Department.

- Funds must be transferred from overseas in foreign currency (USD, EUR, GBP, etc.) and converted to Thai Baht at a Thai bank. Direct transfers in Thai Baht from an overseas account will be rejected by the Land Department.

- The receiving bank then issues a Foreign Exchange Transaction Form (FETF) — previously known as the Thor Tor 3. Without the FETF, you cannot register ownership. In 2026, the SWIFT transfer instructions must explicitly state the purpose (e.g., “For the purchase of Condominium Unit X in Project Y”). Vague transfer memos routinely result in the bank refusing to issue the FETF. For remittances exceeding USD 50,000, an electronic FETF (e-FETF) is standard; for smaller amounts, proactively request a specific credit advice letter from the Thai bank.

- The purchase must be in your name — not a company name, unless the company qualifies under the Foreign Business Act.

Practical tip: Always review the title deed before signing any reservation agreement.

2. Leasehold — For Land, Houses, and Villas

If you want a house, villa, or land, the primary legal pathway is a registered lease under CCC Sections 537–571 and 1336–1337. This is the standard route for foreigners buying a house in Thailand:

- Maximum term: 30 years, registrable at the Land Department

- Must be registered to be enforceable against third parties — unregistered leases above 3 years are void

- The 30+30+30 renewal structure has been definitively struck down by the Supreme Court — do not rely on it

A lease gives you the right to use and enjoy the property, but you do not own the land. The landowner retains the title deed. For a comprehensive guide to structuring your lease correctly, see our lease agreement guide.

What this means in practice: If the landowner dies, goes bankrupt, or sells the land, your lease must be respected by any new owner — but only if it was properly registered. At the expiration of the 30-year term, the lessor has absolute legal discretion over whether to extend or terminate. Even if you pre-paid for extensions, the landlord cannot be compelled to honor them after the Supreme Court ruling. For more on automatic lease renewal issues, see our detailed analysis.

3. Superficies — Building Ownership on Leased Land

Under CCC Sections 1410–1416, a superficies right legally severs the ownership of the land from the ownership of the buildings and structures on it. By default, Section 1337 of the CCC dictates that whoever owns the land also owns everything built upon it. A superficies is a statutory exception to this rule.

By registering a superficies at the Land Office concurrently with a 30-year land lease, the foreign investor gains:

- Freehold ownership of the building — your name appears on the official building permit and the Tabien Baan (House Registration Book) as the undisputed owner of the structure

- Transferability — the right can be sold to third parties or inherited by statutory heirs, providing estate planning security a standard lease lacks

- Renegotiation leverage — if the land lease expires, the landowner cannot simply seize the building without compensating the building owner, giving you significant leverage

This is the closest a foreigner can get to “owning a house” in Thailand without using a company structure. For a comparison of this and other land rights, see our guide on lease, usufruct, and Sap Ing Sith.

4. Usufruct — Lifetime Use Rights

A usufruct (CCC Sections 1417–1428), known in Thai as Sid-thi Keb-kin, grants you the absolute right to possess, use, and enjoy the benefits of a property owned by another person. This mechanism is most commonly used when a Thai spouse purchases property and grants a registered usufruct to their foreign spouse.

- Can last for your entire lifetime (not limited to 30 years), or for a fixed term up to 30 years

- Registered at the Land Department

- Protects you even if the land is sold to a new owner

- You can lease the property to third parties and collect rental income during the usufruct period

- Cannot be inherited — it automatically extinguishes upon your death

A related but more restrictive option is the Right of Habitation (CCC Sections 1402–1409), which grants the right to reside in a building without paying rent. Unlike a usufruct, habitation applies only to the building (not the land), does not permit subletting, and is limited to residential dwelling. However, it is cost-effective to register since the Land Department allows it to be declared with zero compensation, avoiding the leasehold taxes associated with commercial agreements.

5. Section 96 bis — Land Ownership for Major Investors

Under Section 96 bis of the Land Code, a foreigner who invests at least THB 40 million (approximately USD 1.1 million) in approved Thai investments can obtain permission to own up to 1 rai (1,600 sqm) of residential land. This is the only pathway to direct foreign house ownership in Thailand.

The conditions are stringent:

- Capital must be actively invested in government-approved assets — specific Thai government bonds, property funds, or BOI-promoted enterprises — not simply deposited in a bank account

- The investment must be maintained for 3–5 consecutive years, depending on ministerial stipulations active at the time of application

- The land must be in designated zones: Bangkok Metropolitan Administration, Pattaya City, a designated Municipality, or residential zones defined under the Town Planning Act

- Requires comprehensive documentation, background checks, and the explicit approval of the Minister of Interior, endorsed by the Cabinet

- If the investment is disposed of prematurely, the Director-General can revoke the privilege, compelling disposal within 180 days to one year

Due to its restrictive nature and ongoing financial commitments, this option is exceedingly rare — utilized primarily by ultra-high-net-worth individuals and institutional investors.

Ownership Options at a Glance

| Option | Property Type | Duration | Own the Land? | Inheritable? | Best For |

|---|---|---|---|---|---|

| Condo Freehold | Condominiums only | Permanent | No (unit only) | Yes | Simplest, safest option |

| Leasehold | Any (land, house, villa) | Max 30 years | No | Remainder of term | Houses, villas, land use |

| Superficies | Buildings on leased land | Max 30 years | No (building only) | Remainder of term | Combined with lease |

| Usufruct | Any | Lifetime | No | No | Lifetime use, retirees, Thai spouse |

| Habitation | Buildings only | Lifetime | No | No | Residence only, low cost |

| Section 96 bis | Residential land (max 1 rai) | Permanent | Yes | Yes | Ultra-HNW investors (THB 40M+) |

The Risks You Must Know Before Buying Property in Thailand

Nominee Companies: The #1 Trap for Foreign Buyers

The most common — and most dangerous — approach foreigners use is setting up a Thai limited company with nominee Thai shareholders to hold land. By structuring the entity with 51% Thai shareholding and 49% foreign shareholding, the company is technically classified as a “Thai juristic person” and can purchase freehold land. Foreign control is maintained through preferential voting rights, blank share transfer forms, and dominant director powers. This is illegal under the Foreign Business Act B.E. 2542 and the Land Code.

The 2026 enforcement landscape is unprecedented. Led by the Ministry of Commerce and the Department of Business Development (DBD), in collaboration with 17 state agencies — including the Revenue Department, the Anti-Money Laundering Office (AMLO), the Department of Special Investigation, and public prosecutors — the government is executing systematic investigations into over 46,000 companies suspected of operating as illegal nominee structures. We covered this enforcement action in our article on recent crackdowns on nominees in Thailand.

Authorities now conduct “substance over form” investigations, backed by Supreme Court precedents. Investigators make unannounced site visits and interview Thai majority shareholders. If the Thai shareholders cannot produce banking evidence that they genuinely provided their own capital for the share purchase, the structure is immediately classified as illegal.

The most drastic 2026 development: serious Foreign Business Act violations are now classified as predicate offenses under the Anti-Money Laundering Act (AMLA). This empowers AMLO to freeze and seize all assets — including land, villas, and bank accounts — acquired through illicit nominee funding. Penalties include:

- Criminal prosecution: up to 3 years imprisonment and fines of THB 100,000 to THB 1,000,000

- Forced liquidation of the company and permanent revocation of business licenses

- Asset seizure by AMLO under the Anti-Money Laundering Act

- Foreign directors face blacklisting and deportation

We have seen clients lose properties worth millions of Baht. Do not risk it — there are legal alternatives covered above.

Off-Plan Purchase Protections

Since January 31, 2025, the OCPB (Office of the Consumer Protection Board) implemented standardized “controlled reservation contracts” for off-plan condo purchases. These rules ban unfair clauses and standardize the Thai-language contract form — a significant improvement for buyer protection. Make sure your developer complies, and always verify building permits before paying any deposit.

Due Diligence Checklist for Buying Property in Thailand

Before committing any capital to a property transaction, executing comprehensive legal due diligence is non-negotiable. The fundamental lack of standardized escrow services in Thai property transactions makes recovering funds exceptionally difficult once transferred.

| Check | Why It Matters | How to Verify |

|---|---|---|

| Title deed authenticity | Chanote (Nor Sor 4 Jor) is the only full ownership title — other deeds offer weaker rights | Verify at Land Department; learn to read a Thai title deed |

| Encumbrances & mortgages | Existing liens, third-party mortgages, active usufructs, or ongoing litigation can block transfer | Back-page title deed search at Land Dept. |

| Foreign quota status | Condos only — 49% ceiling may already be reached | Official letter from Juristic Person + Land Dept. confirmation |

| Building permits & EIA | Illegal structures can be demolished; coastal and forest zones have building limits | Check with local municipality + Environmental Impact Assessment review |

| Zoning compliance | Property must be zoned for intended use | Verify with local Tessaban or OrBorTor |

| Developer financial health | Off-plan buyers can lose deposits if developer folds | DBD Online (Dept. of Business Development) — check capitalization, litigation history, past project record |

| FETF compliance planning | Without a valid FETF, Land Dept. will reject the condo transfer | Confirm offshore bank can send SWIFT with exact purpose statement; verify Thai bank can issue FETF/e-FETF |

Step-by-Step: How to Buy a Condo in Thailand as a Foreigner

- Sign the Reservation Agreement — Upon selecting a unit, you pay a holding deposit (typically THB 100,000–200,000) to remove the property from the market. This is generally non-refundable unless “subject to clear due diligence” clauses are negotiated by your attorney.

- Engage an independent Thai lawyer — Not the developer’s lawyer. Your counsel handles all due diligence: title verification, seller standing, foreign quota availability, and encumbrance searches.

- Review and sign the Sale and Purchase Agreement (SPA) — Your lawyer scrutinizes and amends the SPA for construction warranties, penalty defaults, and the division of transfer taxes (typically 50/50). Do not sign without legal review.

- Transfer funds from overseas — Wire the remaining purchase price from an offshore bank account in foreign currency. The SWIFT instructions must explicitly state the condominium details.

- Obtain your FETF — The receiving Thai bank converts the funds to Baht and issues the Foreign Exchange Transaction Form. This is the mandatory proof of foreign capital importation.

- Prepare cashier’s cheques — Final balances are settled via official cashier’s cheques payable to the seller. Separate cheques are prepared for the Land Department to cover transfer fees, stamp duty, and taxes.

- Register at the Land Department — You or your lawyer (via Power of Attorney) meets the seller at the local Land Office. Upon presenting your passport, original FETF, signed SPA, and payment of all transfer taxes and fees, the official transfers the Chanote. Update your Thai will to include the new asset.

Costs & Taxes When Buying Property in Thailand

| Fee / Tax | Rate | Paid By | Notes |

|---|---|---|---|

| Transfer fee | 2% of appraised value | Typically split 50/50 | Negotiable between parties |

| Stamp duty | 0.5% | Seller | Only if exempt from SBT |

| Specific Business Tax (SBT) | 3.3% | Seller | If seller owned <5 years |

| Withholding tax | 1% (company) or progressive (individual) | Seller | Deducted at Land Department |

| Lease registration fee | 1% of total rent | Negotiable | For leasehold only |

| Legal fees | THB 30,000 – 150,000+ | Buyer | See our property legal packages |

For a full breakdown of transfer costs, see our property transfer process page.

Frequently Asked Questions About Buying Property in Thailand

Can foreigners own land in Thailand?

Normally no. Under the Thai Land Code (Section 86) and the Civil and Commercial Code, foreigners cannot own land in Thailand. The only exception is Section 96 bis, which allows land ownership up to 1 rai for investors who place at least THB 40 million in approved Thai investments and obtain Cabinet approval. For most buyers, the options are condo freehold, leasehold, usufruct, or superficies — all covered in detail above. There are exceptions too for the BOI and other laws rarely used.

Can I get a mortgage in Thailand as a foreigner?

Traditional Thai banks generally do not offer mortgages to foreign non-residents due to difficulties in recovering offshore assets in case of default. However, foreigners who hold a valid Thai work permit, possess a long-term visa, and can demonstrate stable Thai-taxed income may qualify for domestic financing — typically up to 50–70% LTV. Certain international lenders such as UOB Singapore and MBK Guarantee offer bespoke programs for Thai condominiums, though at rates 1–2% higher than domestic loans. Developer financing over 24–36 months during construction is also a common alternative. A Thaiguarantor can be needed. Mr. Sebastien H. Brousseau, managing director of this law firm got a mortgage so it is possible.

Does buying property give me a Thai visa?

It could be it is rare. Property ownership alone does not grant any immigration status. However, property investment is a qualifying criterion for specific visa categories. In 2026, an investment of USD 500,000 (or USD 250,000 depending on income brackets) in Thai property is a primary pathway to the 10-year Long-Term Resident (LTR) Visa, which provides 10-year residency, tax exemptions on offshore income, and digital work permit privileges. Other long-stay options include the retirement visa, DTV visa, or Thailand Privilege visa. We talk about a New Property Investment Visa here.

Can I rent out my property in Thailand?

Yes — foreigners who legally own a condo freehold or hold a registered leasehold can lease their properties for long-term rentals (over 30 consecutive days). Rental income is subject to Thai personal income tax at progressive rates up to 35%, typically calculated after a 30% statutory expense deduction, yielding net returns of 4–7% depending on location. However, offering short-term rentals (under 30 days) on platforms like Airbnb without a commercial hotel license violates the Hotel Act B.E. 2547 and can result in substantial fines.

What happens to my Thai property when I die?

Thai succession law (CCC Sections 1599–1648) applies to property in Thailand, regardless of your nationality. A foreign heir must pass through Thai probate courts. For condominiums, if the heir doesn’t qualify under the 49% quota or fails to prove new foreign currency importation matching the property’s value, Section 19/7 of the Condominium Act forces the heir to sell the unit within one year. Following January 2026 Ministerial Regulations that standardized identity verification for wills at district offices, foreign property owners are strongly advised to draft a separate, fully compliant Thai will covering their local assets.

What if the 49% foreign quota in a condo is full?

If a condominium project has reached its 49% foreign ownership limit, you are legally barred from acquiring any further units under freehold title. The only alternative is to acquire the unit under a registered leasehold (maximum 30 years) from a Thai owner or developer. While this provides the right to occupy, use, and rent the unit, it does not provide the long-term security of freehold ownership and is subject to the Supreme Court’s non-renewal precedents — making it a significantly less attractive investment vehicle.

Can I transfer land to my Thai spouse or child?

A Thai spouse can own land in their name. Property purchased with marital funds may be considered joint assets under Thai law, but only the Thai spouse’s name can appear on the title. If you have a Thai child, you may also consider transferring land to a Thai child. In both cases, structuring these arrangements with proper legal documentation is essential to protect your financial interests.

What is the difference between a lease and a usufruct?

A lease is limited to 30 years maximum and can include a right to sublease. A usufruct can last for your entire lifetime but ends at death (not transferable to heirs). During the usufruct period, you can lease the property out and collect rental income. Both must be registered at the Land Department to be enforceable. See the comparison table above for a full breakdown of all ownership options.

Conclusion

The Thai property market in 2026 presents a clear paradigm: tightening enforcement against illicit corporate structures, alongside highly secure, legislatively supported opportunities for compliant foreign investment. The multi-agency crackdown on nominee companies and the Supreme Court’s definitive invalidation of “30+30+30” lease renewals signal the end of historical regulatory gray areas.

Conversely, the legal security of the condominium freehold, the practical utility of superficies and usufructs, and the potential horizon of a 99-year leasehold provide robust tools for the informed investor. In a domestic market experiencing tightened local credit availability, foreign buyers with transparent, compliant offshore capital are well-positioned to negotiate premium assets — provided they abandon antiquated legal “shortcuts” and work within proper legal frameworks.

Need expert guidance? ThaiLawOnline.com has helped Western clients navigate Thai property law for over 30 years. Book a property consultation to discuss your specific situation.